The St. Petersburg Paradox

How Daniel Bernoulli's 1738 coin-toss thought experiment with infinite expected value revealed the gap between mathematical rationality and human decision-making, laying the foundations for expected utility theory and modern behavioral economics.

Russian Tsar Peter I, in a very short reign, radically transformed Russia. Among other things, hoping to create a new intellectual center, he founded the Academy of Sciences in his newly built city of St. Petersburg. Prominent European scholars were invited to the Academy, among them the brilliant Swiss mathematicians Euler and two members of the Bernoulli family.

We begin using the fruits of Euler's work as early as school. Many remember "Euler's number" 2.7, the second most famous constant after pi. Or the function notation f(x), also introduced by Euler.

However, this story is about Daniel Bernoulli. In 1738, he published an influential paper titled "Exposition of a New Theory on the Measurement of Risk," in which he described what became known as the St. Petersburg Paradox. The paper became one of the most significant texts ever written on the problems of both risk and human decision-making behavior in general.

But before we examine what the St. Petersburg Paradox is, let each reader decide which button they would press:

On one hand, mathematically the green button is more advantageous — the expected value of choosing the green button is 5 times higher ($10 million x 0.5 > $1 million x 1).

On the other hand, as surveys show, most people would choose the red button because they want to avoid the risk of "returning to zero" associated with the green button. Simply because their fear of losing everything (or receiving nothing) is stronger than their desire for a larger but uncertain reward.

Bernoulli pondered a similar problem. He hypothesized that calculating expected value through mathematical expectation may be insufficient for describing real-life decision-making. Because it accounts only for facts and ignores human behavior when making decisions under uncertainty. Bernoulli believed that while the facts are the same for everyone, the utility in each individual case depends on the person making the assessment. And there is no reason to assume that risk, perceived differently by each individual, can be evaluated identically.

Daniel Bernoulli. A member of the famous Swiss Bernoulli family, which produced outstanding mathematicians and natural scientists over two centuries. He studied at the University of Basel's medical faculty. From 1725 to 1733, he worked at the departments of physiology and mathematics at St. Petersburg University.

The Game

Bernoulli proposed a game. To enter, you pay a certain sum for participation, then flip a coin until heads appears. If heads comes up on the first flip, you receive $2 and the game ends. If tails, you flip again. If heads appears on the second flip, you receive $4; if tails, the game continues. For each subsequent round, the prize for heads doubles ($2, $4, $8, $16, and so on) — you proceed to the next round until heads finally appears.

The question is: what entry fee makes this game fair or acceptable for the player? In simpler terms, we need to find the mathematical expectation of the player's winnings. The paradox is that the calculated value of this fair entry fee equals infinity — that is, it exceeds any possible winning amount. In other words, the essence of the paradox: individuals are willing to pay a relatively small sum (on average, people name $20-30) to participate in a game where the mathematical expectation of winnings is infinitely large.

See for yourself — each round yields an expected gain of $1, and the series looks like this: $2 x 1/2 + $4 x 1/4 + $8 x 1/8, and so on to infinity. Therefore, the mathematical expectation of the player's winnings = $1 + $1 + $1 + $1... = ∞.

The Solution: Expected Utility

Bernoulli hypothesized that in everyday life, individuals strive not to mathematically maximize possible monetary gain, but rather to maximize expected utility — the degree of satisfaction. Expected utility is calculated using the same methods as mathematical expectation, but is evaluated with the weight of the utility factor taken into account.

Imagine that your debtor, instead of returning 1 million rubles to you, proposes a coin flip. If you win, you receive not 1 but 2 million rubles, but if you lose, you receive nothing — meaning you lose your 1 million. The mathematical expectation in this case is: 0.5 x 1 + 0.5 x (-1) = 0.

Consider another example. Suppose you have $100. You can play roulette and bet $50 on red. If you win, you'll have $150: the $50 you didn't bet, plus $50 x 2 — your winnings. Thus you increase your initial wealth of $100 by $50. If you lose, you'll have just $50 — decreasing your initial wealth by $50. The mathematical expectation of winnings in monetary terms is: 0.5 x 50 + 0.5 x (-50) = 0.

The mathematical expectation in both games equals zero — it shouldn't matter whether you play or not. Yet most people still refuse to participate in such games. Practice shows that the vast majority of people are risk-averse. This behavior is typically explained, apart from features of human psychology, by a purely economic reason: the law of diminishing marginal utility.

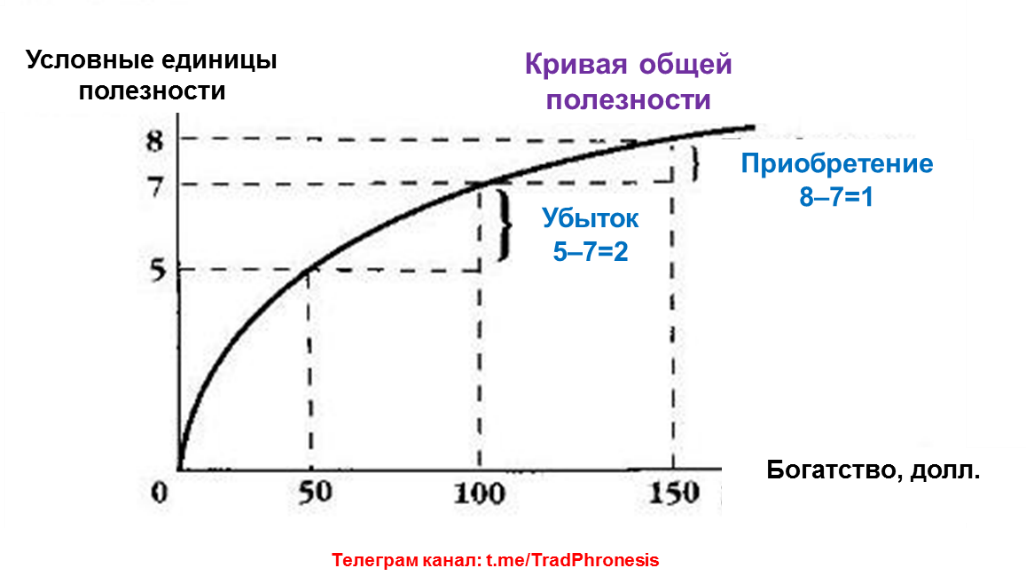

The figure above provides the explanation. Marginal utility, as visible from the total utility graph, is diminishing. Therefore, in conventional utility units, the expected utility of the games described above will have not a zero but a negative value. In the example shown: 0.5 x (-2) + 0.5 x 1 = -0.5.

In case of loss, your losses in utility units will be greater than your gains in case of winning. Thus, in utility terms, the situation looks different from monetary terms calculated through mathematical expectation, and you will not be inclined to take the risk. This is precisely what Bernoulli urged — to distinguish between the mathematical expectation of a monetary sum and its expected utility. Put more simply: of course, we would be happy to receive more than we have, but we feel the loss of what we're accustomed to much more acutely. In behavioral economics, this phenomenon is called the Endowment Effect — people value what they already own much more highly than what they don't yet possess.

One of the founders of behavioral economics, Amos Tversky, once said about the Law of Diminishing Marginal Utility: "The more money someone has, the less they value each additional increment. Or: the utility of any additional dollar decreases with increasing capital."

That is, we value the second thousand we receive less than the first, the third less than the second, and so on.

Back to the Paradox

Returning to the St. Petersburg Paradox, we can now say that individuals who refuse the coin-toss game — despite the infinitely large mathematical expectation — are guided, according to Bernoulli's hypothesis, primarily by the expected utility of their winnings. And the marginal utility of income decreases with each increment.

Bernoulli also showed that people evaluate the same risk differently. He tried to explain this paradox through the marginal utility of money, within which the benefit of wealth increase is inversely proportional to initial wealth. That is, Bernoulli transformed the process of calculating probabilities into a procedure for incorporating subjective considerations into decision-making under uncertain outcomes.

For the first time in history, Bernoulli applied measurement to something that cannot be counted. He connected intuition with measurement. Cardano, Pascal, and Fermat created probability theory and the mathematical method for calculating risk in dice games, but Bernoulli brought us to the risk-taking individual — to the player deciding how much to bet, and whether to bet at all. If probability theory rationalizes choice, then Bernoulli defines the motivation of the person making the choice. He effectively identified a new subject of study and laid the intellectual foundations for what later found application not only in economic theory but in the general theory of decision-making across various life situations.

Legacy and Modern Applications

The concept of utility proved so productive that over the following two centuries it became the primary tool for explaining decision-making processes and choice theory. For example, in Game Theory — the approach to systematic decision-making in war, politics, business, and other fields invented in the mid-20th century by John von Neumann and Oskar Morgenstern. In Game Theory, they showed that under conditions of incomplete information, the rational choice for an individual is the choice with maximum expected utility.

Daniel Bernoulli can also be considered the forefather of Behavioral Economics and Finance, which appeared more than two centuries after his death in the 1970s, at the intersection of traditional finance and psychology. Psychologists Daniel Kahneman and Amos Tversky began studying the peculiarities of thinking and behavior in people making decisions under uncertainty. They proved that human thinking and actions are influenced by so-called cognitive and emotional biases that prevent us from making optimal rational decisions and lead to errors. These biases, commonly grouped under the term "behavioral biases," follow certain patterns that have been identified and well experimentally validated by researchers.

In their research, Kahneman and Tversky established that people take into account not only financial consequences but also emotional ones. It turned out that decision-making is also influenced by the anticipation of regret, along with expectations of other consequences. When making decisions, people strive not to maximize utility but to minimize regret. Thus they formulated Regret Theory.

One of the rules of Regret Theory states: the closer you get to achieving a goal, the greater the regret you feel if you fail to reach it. The second rule: regret is closely tied to a sense of responsibility. The more you can control the outcome of a situation, the greater the regret you feel when things go wrong.

And if we return to the beginning of this post, to the question of choosing the red or green button, Regret Theory explains the choice of the red button. By choosing the guaranteed $1 million, people try to minimize regret in exchange for giving up a bet with higher expected utility.

This is also how most people behave after their portfolio stocks rise by 100% or 200%. It is emotionally easier for us to lock in profits than to continue holding a promising stock. This was the case with owners of Amazon or Nvidia shares and many other companies who sold their stocks years ago after strong growth.

Such is the price people pay to avoid regret.